While there are more tools than ever to help you track and manage your finances, I still find it helps to take a step back and identify your financial goals broadly and for the current year specifically. These goals can help guide you in decision making throughout the year and serve as an accountability check to keep you on track. Perhaps as important, it forces you to think about what your priorities are and to think through what steps you need to take to advance closer to the outcome you are trying to achieve.

By Failing to prepare, you are preparing to fail.

Benjamin Franklin

In pursuing Financial Independence, there are fortunately only a few variables we need to focus on. For that matter, even if FI isn’t your goal, having a plan to maximize these variables will still lead to a more secure financial life.

- Maximize savings

- Eliminate debt

- Lifestyle choices to reduce expenses

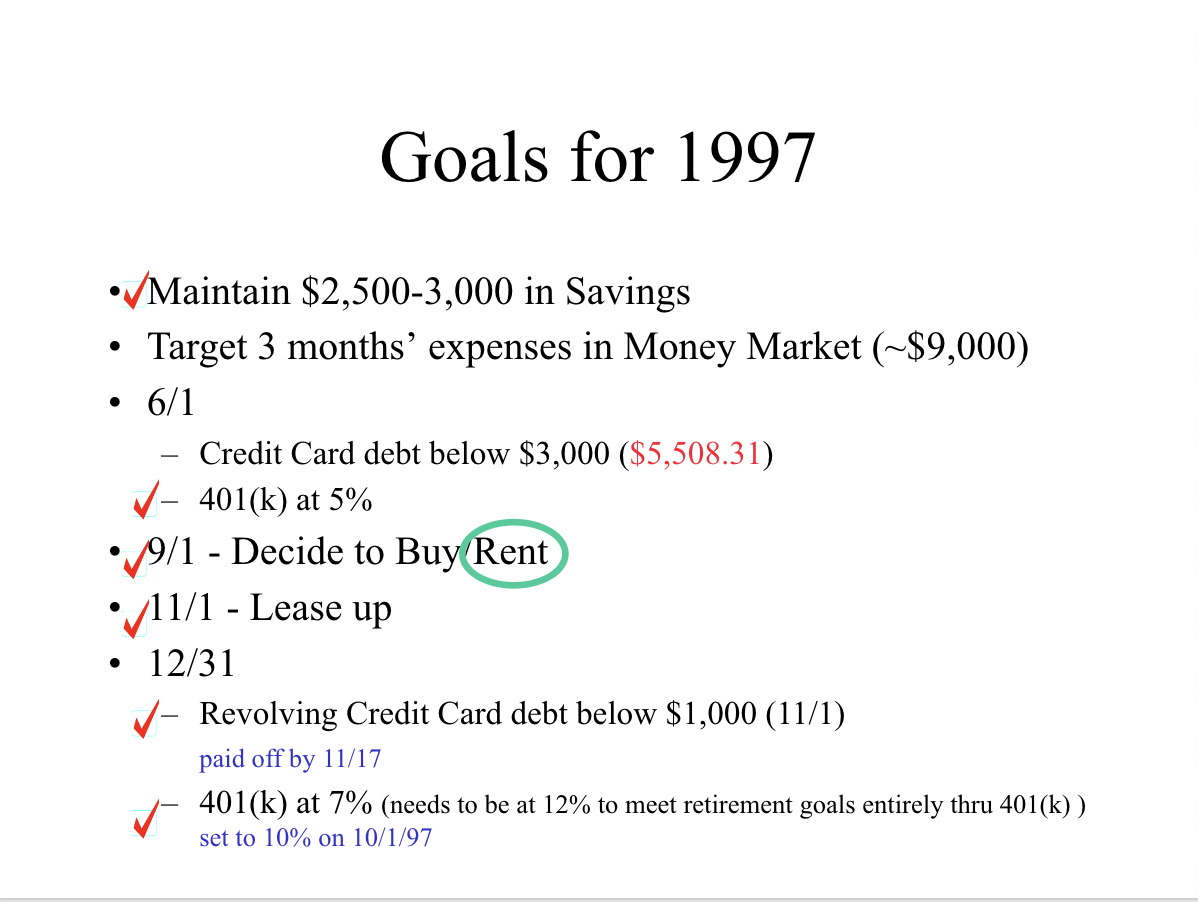

For several years, my wife and I documented our annual financial goals on a single Powerpoint slide, and I can now look back at over a decade of goals and see how we did each year. Below you can see our goals from 1997, along with annotations I made throughout the year to track progress.

This was a powerful way to keep us on the same page as a couple, but also to keep us focused on our goals. You can see above that we didn’t hit our goal of getting our credit card debt below $3,000 by 6/1/1997. That caused us to figure out where to cut back and pay all our credit card debt off by 11/1 a month ahead of schedule.

If you are following a FIRE plan, you’re in luck because really there’s less analysis to do. Unlike most people, you’re NOT trying to figure out what’s the least you need to save in your 401(k) to be able to retire at 67 (for those born in 1960 or later.) You’re building your lifestyle to max out your 401(k) and your HSA, but I still urge you to write it down and do regular reviews of your progress.

When you are making good progress against your plan, that will make you feel great and energized to continue on the path. When you miss your goals, then you will have to face it and figure out what needs to happen to get back on track.

Schwab recently published research showing that “Having a written plan can increase confidence and result in more constructive financial behavior.” This includes a finding that 78% of people with a financial plan pay their bills on time and save regularly, compared to only 38% of those without. As I have written before, and is pretty much obvious anyway, living below your means is the key to Financial Independence and wealth.

That said, you definitely do not need to go out and hire a financial planner, though you certainly can. However, the advice they’ll give is the standard fare you’d get from all of the popular financial press, and not in line with the approach most FIRE adherents are taking. Really what you’d be paying for, in my opinion, is simply the ability to have someone to talk things through with and bounce ideas off of. And if that is what you need to have the confidence in your plans, by all means do so.

For my part, my wife and I have evolved from a simple one page slide to a more detailed written plan in the outline below. Note that we no longer carry any debt and have money set aside for the college, so those goals are no longer part of our plan, but might need to be part of yours.

- Objectives

- Allocation Strategy

- Stock strategy

- International strategy

- Bond funds strategy

- Alternatives (they only alternatives we have in our portfolio are REITs and crypto)

- Cash (not including emergency funds, which we consider outside of our investment portfolio)

- Link to current portfolio and allocation trackers

- Rebalancing plan

- Tax management strategy

- Annual targets for 401(k)s, HSAs, IRAs (we use backdoor Roth IRAs to build a conversion ladder)

Also, here a few other resources to check out that I liked and may help you with developing your own plan. While these are best practices, also make it your own and make it work for you and your particular circumstances:

- 10 Steps to a DIY Financial Plan (Schwab)

- How to Write a Personal Financial Plan (WikiHow)

- Write a Personal Financial Plan in 7 Easy Steps (SmartMoney)

Photo by Helloquence on Unsplash